Saturday, December 8, 2012

Taxes and business

* Joe White, in the Nov 25 Letters to the Tennessean, argues that financial incentives to lure a business to a county or state are analogous to reductions of income-tax and capital-gains tax to enrich the already rich. He claims that the economic benefits for the rest of us outweigh the economic costs to the rest of us.

* I wonder whether an honest accounting of losses and gains in our business-luring programs would support his thesis. What about American Airlines, Dell, the arena, the stadium, etc. My property-taxes have increased painfully since these deals were made. It would be rational for all sub-national governments to agree on a federal law forbidding financial incentives to influence locating of businesses among states and counties. Then businesses would go where their prospects are best, not to where they have been bribed to go. HCA would almost certainly stay in Nashville without a bribe, since its founders, owners and officers have deep roots here.

* Anyone or any business that could naturally be in Nashville but chooses to go elsewhere is giving up the opportunity to be in the most interesting place in the US--an island of intellectual and cultural ferment in a State that rivals paradise.

* Ethically speaking, it doesnn't matter where a business moves. God (ie an objective observer of good will) might care about per capita happiness, not where that happiness happens.

* The idea that tax-paying employees of a business will improve local revenues is flawed, in that those employees must be provided infrastructure and services that consume revenues. Nashville is already too crowded. Try driving on any of our arteries, especially Woodmont Blvd or Harding Pl most hours of the day.

* The prosperity of a community depends on its products and services that are bought by ousiders. Competing for such businesses could be in the self interest of locals.

* Finally, the fees collected from businesses by brokers/consultants for negotiating their tax breaks are obscene, about 30% of the tax break. That offends me.

* I wonder whether Joe White is parroting the Reagan/Laffer narrative or has studied the economic data bearing on his claims about tax cuts.

* The data show that Kennedy's economic boom began in 1968, 3 years before Kennedy took office and 5 years before his tax cut, which had no discernible effect on revenues. After the Reagan tax cuts, revenues abruptly fell about 20% below their pre-Reagan trajectory, continued drifting down from that trajectory until 1993, then began rising when the top income-tax rate rose from 30% to 40%. This revenue rise was broken in 2001, due to financial turmoil following the 9/11 attacks, then returned in 2004 after the 2003 tax cuts but in fact due to a housing bubble that popped three years later. We have little to show for tax cuts except our ballooned government debt.

Monday, November 12, 2012

US Macroeconomic History

I've been assembling macroeconomic data to explore influences of independent variables (tax rates, government spending, oil prices, interest rates, regulations) on dependent variables (inflation, prosperity, employment, government debt, wealth distribution). They are presented in this essay. What do you see?

* GDP grew in three main phases, slow, fast and slow, corresponding to phases of CPI growth, inflation being the dominant component of GDP growth. The GDP growth in excess of inflation and population growth represents supra-subsistance purchase of goods and services, ie prosperity or life style. US prosperity in the present decade (2002-2012) is about twice that in the 1950s. Why aren't we grateful? Probably because most of the increased prosperity was for the richest citizens; little of the increased prosperity was shared by average workers -- this shown in the Top 1% Income Share plot of Fig 4. The dynamics of wealth distribution are examined by Robert Reich.

* Comparing Figs 1 and 2, one sees that prosperity declined between 1978 and 1982, when oil prices and interest rates were highest and GDP growth was fastest; and prosperity improved between 1982 and 1988 when oil prices and interest rates were falling, government spending was elevated and GDP growth was slowing. Given these data, one cannot attribute the Reagan prosperity to tax cuts, and one cannot look to GDP growth as a measure economic health. Do economists, pundits and politicians know this?

* There are some (but not enough) negative-feedback loops from dependent variables back to independent variables, antagonizing departures from a steady state--in the face of economic disturbances such as technological advances, international trade, educational outcomes, wars, resource variations, immigration, social justice, labor movements, etc. The feedbacks may be market forces (prosperity back to oil price), interventions (inflation and employment rate back to interest rates, government debt back to tax rates and government spending), regulatory (resource reserves and environment back to exploitation). Political doctrines distort these feedbacks.

* Employment rate (inverse of unemployment rate shown in Fig 2) is seen as a more sensitive and reliable index of economic health than prosperity shown in Fig 1. Nevertheless, comparing the two, one sees that the prosperity plot is meaningful. For example, the long employment recovery from 1958 to 1968 corresponds to a steeper prosperity rise from 1960 to 1969, likewise for 1982 to 1988 and other intervals.

* The unemployment plot looks almost like a delayed version of the interest-rate plot (CMT = Constant Maturity Treasury), and it looks almost like a delayed version of the oil-price plot in direction though not in amplitude. One can even see a correlation between government spending and economic health. Given these apparent dynamics regardless of tax rates, I conclude that the 1980s recovery would surely have occurred without the tax cuts, whose undeniable effects were massive government debt and social imbalance.

Prior to the tax cuts and spending increases of the 1980s, government debt relative to GDP declined. During the 1980 presidential campaign, Reagan (reportedly based on Laffer's theory) claimed that he could balance the budget while cutting taxes and increasing military spending. Fig 3 shows that his claim was false. Today's irrational national conversation about taxes and spending is the Reagan/Laffer legacy.

Prior to the tax cuts and spending increases of the 1980s, government debt relative to GDP declined. During the 1980 presidential campaign, Reagan (reportedly based on Laffer's theory) claimed that he could balance the budget while cutting taxes and increasing military spending. Fig 3 shows that his claim was false. Today's irrational national conversation about taxes and spending is the Reagan/Laffer legacy.

* As seen in Fig 4, Reagan's tax/spending policies increased the income share of the already wealthy, the richest 1% of Americans now getting 18% of income, a 2.25x increase from pre-Reagan years. The average 1%er now receives 25x what the average 99%er receives, ie the average 1%er receives about $500/hour or $4000/day. (Is this correct?) This was a deliberate policy to increase capital formation for the sake of entrepreneurialism. My experience is that businesses start and grow when paying customers have unmet needs and desires. More capital sloshing among the hedge funds contributes little if anything to economic health.

* Rich people don't know what's good for them. When they take power and rig tax rates to enrich themselves at the expense of budget balance, they don't feel satisfied, since their increased wealth gets them little they couldn't already afford and their social peers grow richer with them as a cohort. If at the same time they do nothing for average citizens, they are condemned as greedy. With all that power, they failed to arrange a just sharing of the benefits of technology with and among laborers. Now that everyone has smart phones and social media, there is a growing risk of civil unrest. Carried interest could become the cause celebre of unemployed and demoralized workers demanding restoration of economic justice.

* Laborers don't know what's good for them. They blackmail managers into wages and benefits that may not be sustainable. They should accept a base-pay/profit-sharing formula that ensures that their jobs endure as long as possible, in America.

* Fig 5 shows reveneues and expenditures causing the debt seen already in Fig 3. In passing, it is worth noting that we got through the Korean War, Vietnam War and the Great Society with modest revenues, modest expenditures, modest deficits, relatively good employment and declining debt/GDP. It seems to me that Reagan's tax cuts might have been a simple-minded response to more people earning into the highest bracket and complaining about it to their government buddies, top rate being 70%, this resulting in revenues 20% of GDP. It would have been better to leave the tax rates unchanged and to index the tax brackets to CPI so as to move revenues toward 20% of GDP, where it would have prevented the unbridled growth of debt. Any scientist or engineer could accomplish this if so commissioned, but Congress cannot be trusted to do it. The effects of this fine tuning are shown in the green Debt plot, where it is seen that our debt/GDP today would be a manageable half what it actually is, less than twice what it was in 1980. Without the housing-bubble collapse of 2007, government debt would be only 30% of GDP as it was before Reagan's tax cuts.

* Now, what about that Fiscal Cliff. As argued above, the 1980s recovery could be explained by falling interest rates, falling oil prices and increased spending, one or more of these initiating every recovery. While tax cuts might have contributed to the recovery, there is no evidence that they did. The even bigger recovery of the 1990s was again anticipated by falling interest rates, falling oil prices and some extra spending. The increases of income tax rate and capital-gains tax rate of the late 80s and early 90s clearly did not constitute a fiscal cliff. And the tax cuts of the early 2000s did not prevent the economic collapse of 2007. Since government debt is getting to be a serious problem and since there is no evidence that tax cuts ever had a beneficial effect or that tax hikes ever had a harmful effect on economic health, we should let the Bush tax cuts expire for all earning more than $100k/y or for everybody.

* With a model accounting for the influence of independent variables on dependent variables, one could estimate the sensitivity of any dependent variable to any independent variable. The above considerations support the view that economic-health measures (employment, prosperity) are extremely insensitive to tax rates. Any detrimental effect of the expected tax hike on economic health could be easily compensated by a modest regulatory or spending adjustment.

* The looming economic threat is not a tax hike; it's the European cash-flow imbalance that might lead to a sudden drop in European buying power.

Update: A 2017 expert analysis essentially agrees with the above, as does a more recent one.

David M Regen

Recreational Utopian

xmsdavidr@gmail.com

* GDP grew in three main phases, slow, fast and slow, corresponding to phases of CPI growth, inflation being the dominant component of GDP growth. The GDP growth in excess of inflation and population growth represents supra-subsistance purchase of goods and services, ie prosperity or life style. US prosperity in the present decade (2002-2012) is about twice that in the 1950s. Why aren't we grateful? Probably because most of the increased prosperity was for the richest citizens; little of the increased prosperity was shared by average workers -- this shown in the Top 1% Income Share plot of Fig 4. The dynamics of wealth distribution are examined by Robert Reich.

* Comparing Figs 1 and 2, one sees that prosperity declined between 1978 and 1982, when oil prices and interest rates were highest and GDP growth was fastest; and prosperity improved between 1982 and 1988 when oil prices and interest rates were falling, government spending was elevated and GDP growth was slowing. Given these data, one cannot attribute the Reagan prosperity to tax cuts, and one cannot look to GDP growth as a measure economic health. Do economists, pundits and politicians know this?

* There are some (but not enough) negative-feedback loops from dependent variables back to independent variables, antagonizing departures from a steady state--in the face of economic disturbances such as technological advances, international trade, educational outcomes, wars, resource variations, immigration, social justice, labor movements, etc. The feedbacks may be market forces (prosperity back to oil price), interventions (inflation and employment rate back to interest rates, government debt back to tax rates and government spending), regulatory (resource reserves and environment back to exploitation). Political doctrines distort these feedbacks.

* Employment rate (inverse of unemployment rate shown in Fig 2) is seen as a more sensitive and reliable index of economic health than prosperity shown in Fig 1. Nevertheless, comparing the two, one sees that the prosperity plot is meaningful. For example, the long employment recovery from 1958 to 1968 corresponds to a steeper prosperity rise from 1960 to 1969, likewise for 1982 to 1988 and other intervals.

* The unemployment plot looks almost like a delayed version of the interest-rate plot (CMT = Constant Maturity Treasury), and it looks almost like a delayed version of the oil-price plot in direction though not in amplitude. One can even see a correlation between government spending and economic health. Given these apparent dynamics regardless of tax rates, I conclude that the 1980s recovery would surely have occurred without the tax cuts, whose undeniable effects were massive government debt and social imbalance.

* As seen in Fig 4, Reagan's tax/spending policies increased the income share of the already wealthy, the richest 1% of Americans now getting 18% of income, a 2.25x increase from pre-Reagan years. The average 1%er now receives 25x what the average 99%er receives, ie the average 1%er receives about $500/hour or $4000/day. (Is this correct?) This was a deliberate policy to increase capital formation for the sake of entrepreneurialism. My experience is that businesses start and grow when paying customers have unmet needs and desires. More capital sloshing among the hedge funds contributes little if anything to economic health.

* Rich people don't know what's good for them. When they take power and rig tax rates to enrich themselves at the expense of budget balance, they don't feel satisfied, since their increased wealth gets them little they couldn't already afford and their social peers grow richer with them as a cohort. If at the same time they do nothing for average citizens, they are condemned as greedy. With all that power, they failed to arrange a just sharing of the benefits of technology with and among laborers. Now that everyone has smart phones and social media, there is a growing risk of civil unrest. Carried interest could become the cause celebre of unemployed and demoralized workers demanding restoration of economic justice.

* Laborers don't know what's good for them. They blackmail managers into wages and benefits that may not be sustainable. They should accept a base-pay/profit-sharing formula that ensures that their jobs endure as long as possible, in America.

* Fig 5 shows reveneues and expenditures causing the debt seen already in Fig 3. In passing, it is worth noting that we got through the Korean War, Vietnam War and the Great Society with modest revenues, modest expenditures, modest deficits, relatively good employment and declining debt/GDP. It seems to me that Reagan's tax cuts might have been a simple-minded response to more people earning into the highest bracket and complaining about it to their government buddies, top rate being 70%, this resulting in revenues 20% of GDP. It would have been better to leave the tax rates unchanged and to index the tax brackets to CPI so as to move revenues toward 20% of GDP, where it would have prevented the unbridled growth of debt. Any scientist or engineer could accomplish this if so commissioned, but Congress cannot be trusted to do it. The effects of this fine tuning are shown in the green Debt plot, where it is seen that our debt/GDP today would be a manageable half what it actually is, less than twice what it was in 1980. Without the housing-bubble collapse of 2007, government debt would be only 30% of GDP as it was before Reagan's tax cuts.

* Now, what about that Fiscal Cliff. As argued above, the 1980s recovery could be explained by falling interest rates, falling oil prices and increased spending, one or more of these initiating every recovery. While tax cuts might have contributed to the recovery, there is no evidence that they did. The even bigger recovery of the 1990s was again anticipated by falling interest rates, falling oil prices and some extra spending. The increases of income tax rate and capital-gains tax rate of the late 80s and early 90s clearly did not constitute a fiscal cliff. And the tax cuts of the early 2000s did not prevent the economic collapse of 2007. Since government debt is getting to be a serious problem and since there is no evidence that tax cuts ever had a beneficial effect or that tax hikes ever had a harmful effect on economic health, we should let the Bush tax cuts expire for all earning more than $100k/y or for everybody.

* With a model accounting for the influence of independent variables on dependent variables, one could estimate the sensitivity of any dependent variable to any independent variable. The above considerations support the view that economic-health measures (employment, prosperity) are extremely insensitive to tax rates. Any detrimental effect of the expected tax hike on economic health could be easily compensated by a modest regulatory or spending adjustment.

* The looming economic threat is not a tax hike; it's the European cash-flow imbalance that might lead to a sudden drop in European buying power.

Update: A 2017 expert analysis essentially agrees with the above, as does a more recent one.

David M Regen

Recreational Utopian

xmsdavidr@gmail.com

Monday, October 22, 2012

Fiscal Cliff or Fiscal Reform?

* I've been examining the past half century of macroeconomic data, because the national conversation about tax rates, economic health and employment seemed suspect.

* I've come to believe that gross domestic product (GDP) is not a valid measure of economic health, and its growth is not universally desirable. To a good approximation, GDP growth in recent decades is 15% population growth, 67% inflation, and 18% prosperity growth--as seen in this graph:

Those of us who care about the planet don't cheer for population growth. Those of us hoping for some dignity in retirement don't cheer for inflation. And since Republicans took power in 1980, essentially all prosperity growth has gone to the advantaged, this not to be praised by laborers, minorities and those of us wishing for more justice and balance.

Those of us who care about the planet don't cheer for population growth. Those of us hoping for some dignity in retirement don't cheer for inflation. And since Republicans took power in 1980, essentially all prosperity growth has gone to the advantaged, this not to be praised by laborers, minorities and those of us wishing for more justice and balance.

* I've come to believe that the only macroeconomic variable worth cheering for is employment rate. There have been four substantial employment-rate recoveries in the past half century and two minor ones, these depicted in the over-struck phases of the unemployment plot in following graph:

Three substantial recoveries began during long periods of constant tax rates (income, capital gains, inheritance). One of them began after tax-rate reductions but also after large reductions of oil price from a stifling $100/barrel and of constant-maturity-treasury (CMT) interest rate from a stifling 20%, at a time when we still made much of what we consumed and so were hungry for credit. In fact, all employment recoveries followed interest-rate reductions and/or oil-price reductions. Interest rates are now negligible, so we need to explore new actions to increase employment rate without harmful side effects.

Three substantial recoveries began during long periods of constant tax rates (income, capital gains, inheritance). One of them began after tax-rate reductions but also after large reductions of oil price from a stifling $100/barrel and of constant-maturity-treasury (CMT) interest rate from a stifling 20%, at a time when we still made much of what we consumed and so were hungry for credit. In fact, all employment recoveries followed interest-rate reductions and/or oil-price reductions. Interest rates are now negligible, so we need to explore new actions to increase employment rate without harmful side effects.

* In passing, note that the prosperity curve declined between 1978 and 1982, the period of peak oil price and peak CMT interest rate. It also declined between 2007 and 2009, when oil price again peaked and the housing bubble popped. Prosperity trends would be hard to identify in real time. It is interesting also that the CPI curve shows a phase of high inflation between 1968 and 1982, especially after 1973. Back then I attributed this to a strong labor movement and OPEC.

* There is not a scintilla of evidence supporting the hypothesis that cutting income, capital-gains and inheritance tax rates benefits average Americans. Tax cuts increased national budget deficits, increased national debt and enriched the rich--claims from the Business Round Table, Heritage Foundation, Cato Institute and local economists notwithstanding. This transfer of wealth from treasury to the privileged can be appreciated from the following two graphs:

*From http://www.usgovernmentspending.com:

Observe the climb of government debt relative to GDP following Reagan's reductions of income and capital-gains tax rates and his increase of spending relative to GDP.

Observe the climb of government debt relative to GDP following Reagan's reductions of income and capital-gains tax rates and his increase of spending relative to GDP.

*From Fred the Oyster at commons.wikipedia.org:

Observe the climb of Top 1% income share after Reagan's tax-rate reductions and spending increases. Both government debt and Top 1% income share rose again after Bush II's tax cuts.

Observe the climb of Top 1% income share after Reagan's tax-rate reductions and spending increases. Both government debt and Top 1% income share rose again after Bush II's tax cuts.

* Next time someone claims economic benefits of tax cuts, please insist that they show you the data!

* Two recommendations emerge from these considerations: 1) Since the Bush tax cuts transferred money from the US Treasury to already rich people without improving economic health, Obama should let them all expire during the lame-duck period regardless of protests from the business world and regardless of his own four-year-old campaign rhetoric. 2) By decree or statute, all multistate retailers should be required to increase their US manufacturing labor expenditure by 1% of their foreign manufacturing labor expenditure after any year in which our unemployment rate averages above 7%--this constituting a walmartization-limiting negative feedback loop. There are several other innocuous tweaks that would improve the US employment rate.

* I've come to believe that gross domestic product (GDP) is not a valid measure of economic health, and its growth is not universally desirable. To a good approximation, GDP growth in recent decades is 15% population growth, 67% inflation, and 18% prosperity growth--as seen in this graph:

* I've come to believe that the only macroeconomic variable worth cheering for is employment rate. There have been four substantial employment-rate recoveries in the past half century and two minor ones, these depicted in the over-struck phases of the unemployment plot in following graph:

* In passing, note that the prosperity curve declined between 1978 and 1982, the period of peak oil price and peak CMT interest rate. It also declined between 2007 and 2009, when oil price again peaked and the housing bubble popped. Prosperity trends would be hard to identify in real time. It is interesting also that the CPI curve shows a phase of high inflation between 1968 and 1982, especially after 1973. Back then I attributed this to a strong labor movement and OPEC.

* There is not a scintilla of evidence supporting the hypothesis that cutting income, capital-gains and inheritance tax rates benefits average Americans. Tax cuts increased national budget deficits, increased national debt and enriched the rich--claims from the Business Round Table, Heritage Foundation, Cato Institute and local economists notwithstanding. This transfer of wealth from treasury to the privileged can be appreciated from the following two graphs:

*From http://www.usgovernmentspending.com:

*From Fred the Oyster at commons.wikipedia.org:

* Next time someone claims economic benefits of tax cuts, please insist that they show you the data!

* Two recommendations emerge from these considerations: 1) Since the Bush tax cuts transferred money from the US Treasury to already rich people without improving economic health, Obama should let them all expire during the lame-duck period regardless of protests from the business world and regardless of his own four-year-old campaign rhetoric. 2) By decree or statute, all multistate retailers should be required to increase their US manufacturing labor expenditure by 1% of their foreign manufacturing labor expenditure after any year in which our unemployment rate averages above 7%--this constituting a walmartization-limiting negative feedback loop. There are several other innocuous tweaks that would improve the US employment rate.

Wednesday, September 26, 2012

Economic Dynamics

* The Republican propaganda machine has spent much of every day and night for three years blaming Obama for the slow economic recovery. I would argue that presidents deserve little praise or blame for economic swings during their terms. In case of the latest downturn, conventional tools for economic stimulation had been spent before Obama's tenure.

* Time courses of several economic swings are beautifully illustrated in a couple of graphs published on the web by Bill McBride. Seen in his graphs, the Great Depression was by far the deepest and longest period of job loss. Downturns between 1948 and 1980 were rather short lived. Then each subsequent downturn (1981, 1990, 2001 and 2007) was longer than the previous one. The first three of these were shallow, reflecting the responsiveness of economic activity to reductions of Federal Reserve interest rates. We grew complacent with the apparent ability of the Fed to prevent large recessions.

* Then came the catastrophic recession of 2007, which involved several bank failures. After several desperate actions to stop the bleeding, employment slowly improved and continued improving slowly until the present.

* The slowness of employment recovery in the present recession is due primarily to two facts: 1) Interest rates were already so low that lowering them had little effect, and 2) Businesses won't borrow to expand with fewer than normal customers and orders. In other words, economic actors weren't in a position to respond to a push from slightly easier borrowing. The economy hasn't been capital limited for decades.

* There is reason to fear an interruption of our slow recover, ie a second dip. This is due to imbalance among European countries, who are experiencing bail-out fatigue, and to maturing of the Chinese economy, which can't go on with infrastructure projects forever.

* Most of these factors are out of the president's control. However, there are outside-the-box policies that could get our economy back to a satisfactory steady state.

* Time courses of several economic swings are beautifully illustrated in a couple of graphs published on the web by Bill McBride. Seen in his graphs, the Great Depression was by far the deepest and longest period of job loss. Downturns between 1948 and 1980 were rather short lived. Then each subsequent downturn (1981, 1990, 2001 and 2007) was longer than the previous one. The first three of these were shallow, reflecting the responsiveness of economic activity to reductions of Federal Reserve interest rates. We grew complacent with the apparent ability of the Fed to prevent large recessions.

* Then came the catastrophic recession of 2007, which involved several bank failures. After several desperate actions to stop the bleeding, employment slowly improved and continued improving slowly until the present.

* The slowness of employment recovery in the present recession is due primarily to two facts: 1) Interest rates were already so low that lowering them had little effect, and 2) Businesses won't borrow to expand with fewer than normal customers and orders. In other words, economic actors weren't in a position to respond to a push from slightly easier borrowing. The economy hasn't been capital limited for decades.

* There is reason to fear an interruption of our slow recover, ie a second dip. This is due to imbalance among European countries, who are experiencing bail-out fatigue, and to maturing of the Chinese economy, which can't go on with infrastructure projects forever.

* Most of these factors are out of the president's control. However, there are outside-the-box policies that could get our economy back to a satisfactory steady state.

Friday, September 21, 2012

Economic growth and economic health

* Almost every day a current-events broadcast has someone prescribing more economic growth as a cure for some of America's troubles. I wonder whether there is a definition of economic growth that authorities can agree on. I'll bet that most pundits think that economic growth is GDP growth and that GDP growth is a measure of economic health.

* In fact GDP growth is largely a product of population growth and inflation, neither of which is universally desired. Those of us who feel an ethical obligation to future generations should be imagining, discussing and seeking a society that functions satisfactorily without population growth and with minimal inflation.

* GDP is a normalizing reference or denominator for numerous macroeconomic variables, such as tax revenues, government spending, market indices and especially national debt. For example, lenders' confidence in government bonds depends on (national debt)/GDP. But GDP and its growth is not economic health. In a developed society, one that produces plenty of what it needs, the most reliable expression of economic health is employment rate which is: 100 minus unemployment rate as percentage. In my opinion, this measure of economic health can be nudged to a satisfactory value by several small tweaks in public policy.

* Since GDP growth is mostly population growth and inflation, I postulate that growth of GDP/(population x CPI) should be a pure expression of what's desirable about economic growth. Population is measured only once per decade, so one must interpolate population to estimate this index annually. As seen in Fig 1, 0.1*GDP/(Pop*CPI) passes through 1.0 in 1960, so it is named "Prosperity relative to that in 1960". I calculated this "Prosperty rel 1960" for the past 6 decades and found something interesting.

Over this period, 0.1*GDP/(Pop*CPI) increased 2.47x (from 0.88 to 2.17).

Over this period, 0.1*GDP/(Pop*CPI) increased 2.47x (from 0.88 to 2.17).

* The important result is that Americans on average have well over twice the buying power of their grandparents. That is, we average people could save over half our incomes if we kept our appetites for stuff down to that of our grandparents, or we could use over half our incomes for nonessentials. Everybody who feels that rich hold up your hands. The increased buying power is due to technology and exploitation of poor foreigners holding down inflation.

* The problem is that this extra wealth has gone to the top 10% of Americans, none of it went to the bottom 90%, and the bottom 30% are poorer. If the increase of average buying power was indeed confined to the top 10%, then their buying power would have increased 25 fold. What did they do to deserve that? The wealth is obvious in southwest Davidson Co and Williamson Co. Perfectly good homes were razed to make way for McMansions, and new homes are super mansions--drive down Tyne Blvd, Hillsboro Rd and Franklin Rd.

* Should we discuss the ethical implications of the modern distribution of wealth? Is it right to leave the bottom fifth of our population out of productive employment when we are awash in money? Is failure to share life's satisfactions sinful? Is greed on the rise? What happened to noblesse oblige? This ain't my Utopia. Is it your Kingdom of God?

* In fact GDP growth is largely a product of population growth and inflation, neither of which is universally desired. Those of us who feel an ethical obligation to future generations should be imagining, discussing and seeking a society that functions satisfactorily without population growth and with minimal inflation.

* GDP is a normalizing reference or denominator for numerous macroeconomic variables, such as tax revenues, government spending, market indices and especially national debt. For example, lenders' confidence in government bonds depends on (national debt)/GDP. But GDP and its growth is not economic health. In a developed society, one that produces plenty of what it needs, the most reliable expression of economic health is employment rate which is: 100 minus unemployment rate as percentage. In my opinion, this measure of economic health can be nudged to a satisfactory value by several small tweaks in public policy.

* Since GDP growth is mostly population growth and inflation, I postulate that growth of GDP/(population x CPI) should be a pure expression of what's desirable about economic growth. Population is measured only once per decade, so one must interpolate population to estimate this index annually. As seen in Fig 1, 0.1*GDP/(Pop*CPI) passes through 1.0 in 1960, so it is named "Prosperity relative to that in 1960". I calculated this "Prosperty rel 1960" for the past 6 decades and found something interesting.

* The important result is that Americans on average have well over twice the buying power of their grandparents. That is, we average people could save over half our incomes if we kept our appetites for stuff down to that of our grandparents, or we could use over half our incomes for nonessentials. Everybody who feels that rich hold up your hands. The increased buying power is due to technology and exploitation of poor foreigners holding down inflation.

* The problem is that this extra wealth has gone to the top 10% of Americans, none of it went to the bottom 90%, and the bottom 30% are poorer. If the increase of average buying power was indeed confined to the top 10%, then their buying power would have increased 25 fold. What did they do to deserve that? The wealth is obvious in southwest Davidson Co and Williamson Co. Perfectly good homes were razed to make way for McMansions, and new homes are super mansions--drive down Tyne Blvd, Hillsboro Rd and Franklin Rd.

* Should we discuss the ethical implications of the modern distribution of wealth? Is it right to leave the bottom fifth of our population out of productive employment when we are awash in money? Is failure to share life's satisfactions sinful? Is greed on the rise? What happened to noblesse oblige? This ain't my Utopia. Is it your Kingdom of God?

Wednesday, September 19, 2012

Reaganistic dynamics not confirmed

* In a Sept 7 Tennessean Letter to the Editor, Donnie Allen claimed that the economic success under Clinton was due to a cut in the capital-gains tax rate (Reaganomics), specifically that Clinton's economic improvement started in 1995, the year when the capital-gains tax was reduced from 29% to 15%. These data are wrong, as can be seen comparing a plot of unemployment-rate history with a table of capital-gains-tax history.

.jpg){kind=link}

* In fact, employment began a steady improvement in 1992, when the capital-gains tax had been 29% for five years and would remain so until being reduced to 21% in 1997. The economic improvement was largely due to a tech boom that continued until 2001, when it deteriorated rapidly as the .com bubble popped and Al Qaeda attacked us.

* There were three earlier periods of substantial economic improvement in the past half century. The first began about 1960, in the middle of a two-decade period of 25% capital-gains tax. Space-race spending may have contributed. Another improvement began in 1975, five years into a nine-year period of 35% capital-gains tax. This may have been due to a real-estate bubble that popped after 1980. Another improvement began in 1983, two years after the tax rate was lowered from 29% to 20%. This timing is consistent with Reaganistic theory; but the improvement was almost certainly due to steep reductions of interest rates after the economy had been spring-loaded by years of above-15% interest rates. Falling oil prices helped.

* The data fail to support Reaganistic theory because our economic health hasn't been capital-limited for the past half century. Reagan's tax cuts served only to enrich the already rich, thereby growing the hedge-fund industry.

Monday, September 3, 2012

Republican hatefulness

* Sue Heilman (Aug 23, Tennessean Letters) complains that Republicans have an undeserved reputation for hatefulness, just because they disagree with liberals on issues.

* I know Republicans. Some of my best friends are Republicans (as are my smartest kin). Not one has repudiated or apologized for Rush Limbaugh--the mind and heart of today's conservative movement now dominating the Republican party, who regularly characterizes me and my peeps as vile and despicable, who encourages non-renewable-resource profligacy out of hate for Al Gore and for my grandchildren, who has an insulting name (nazi, socialist, communist) for those in need of justice (labor, women, blacks, gays, poor) and those seeking to extend justice (liberals, progressives, Democrats), who says that our president hates America and whites and is destroying our economy. He uses a variety of deceptive devices to engender hate for progressives, including straw-man arguments, where he attacks Democrats for attributes that he falsely assigns to them.

* All hosts on Fox News Radio (AM 1510) are similarly hateful and deceptive. It was Steve Gill who called Obama a vile and despicable or contemptible nit wit early in 2009, intentionally squandering an opportunity for some redemption in our society.

Monday, April 23, 2012

Reaganistic economist deceives

* During the Mar 9 episode of NPR's "Need to Know", Dan Mitchell of the Cato Institute claimed that Reagan's tax cuts for the rich resulted in a 5x increase of tax revenues from people earning over $200k between 1980 and 1988 (see Reagan tax cuts ). This is a version of the effect predicted by Arthur Laffer, oft cited by Tennessean columnist Richard J Grant of the Beacon Center of Tennessee (see Laffer Curve ).

* The claim seemed paradoxical, since I knew that Reagan's tax cuts resulted in a 20% fall of revenue/GDP and GDP growth slowed under Reagan, owing to slower inflation incident to falling oil prices as OPEC lost discipline (see Reagan's legacy ).

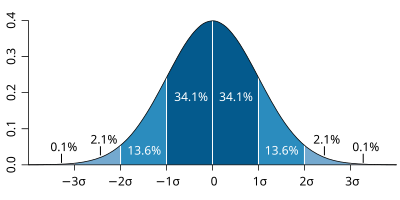

* In fact, there was a 5x increase in revenue from returns reporting more than $200k due to inflation, not tax cuts. The number of returns reporting more than $200k increased 6x because of the 40% inflation between 1980 and 1988 together with the bell shape of the income distribution curve (concave up at the high end). In 1980, only 0.12% of returns reported incomes exceeding $200k, this being 3 standard deviations above the mean (see Standard deviation diagram ). The 40% inflation then spread the distribution rightward so that $200k fell about 2.2 standard deviations above the mean, with about 1.4% of returns expected to report income above $200k. Said another way, in 1980 there was a pool of incomes just below $200k that was more than 10 times the total above $200k. Inflation pushed about 1/2 of that pool above $200k.

* Thus, contrary to claims of the Reaganistic economists, the increased revenue from returns reporting more than $200k income was due to inflation, not due to tax cuts. Had Mitchell carried out a similar analysis on the years from 1972 to 1980, with $100k as the cutoff point, he would have seen a more amazing increase of revenues from incomes above $100k, since the CPI doubled between 1972 and 1980.

* We could learn much about the matter at hand if income-distribution curves were available for the beginning and end of every presidency beginning back in the 1950s.

* The claim seemed paradoxical, since I knew that Reagan's tax cuts resulted in a 20% fall of revenue/GDP and GDP growth slowed under Reagan, owing to slower inflation incident to falling oil prices as OPEC lost discipline (see Reagan's legacy ).

* In fact, there was a 5x increase in revenue from returns reporting more than $200k due to inflation, not tax cuts. The number of returns reporting more than $200k increased 6x because of the 40% inflation between 1980 and 1988 together with the bell shape of the income distribution curve (concave up at the high end). In 1980, only 0.12% of returns reported incomes exceeding $200k, this being 3 standard deviations above the mean (see Standard deviation diagram ). The 40% inflation then spread the distribution rightward so that $200k fell about 2.2 standard deviations above the mean, with about 1.4% of returns expected to report income above $200k. Said another way, in 1980 there was a pool of incomes just below $200k that was more than 10 times the total above $200k. Inflation pushed about 1/2 of that pool above $200k.

{kind=link}

{kind=link}

* Thus, contrary to claims of the Reaganistic economists, the increased revenue from returns reporting more than $200k income was due to inflation, not due to tax cuts. Had Mitchell carried out a similar analysis on the years from 1972 to 1980, with $100k as the cutoff point, he would have seen a more amazing increase of revenues from incomes above $100k, since the CPI doubled between 1972 and 1980.

* We could learn much about the matter at hand if income-distribution curves were available for the beginning and end of every presidency beginning back in the 1950s.

Wednesday, February 29, 2012

Reagan's legacy

(After posting this essay, I decided to analyze US Macroeconomic History, which illustrates several quantitative claims herein. Links to relevant figures were added to this essay.)

* Conventional wisdom holds that Jimmy Carter failed as president and Ronald Reagan succeeded. At the time, it seemed to me that Carter interpreted circumstances objectively, spoke candidly, understood economic dynamics, and steered the nation appropriately into the future. It seemed to me that Reagan interpreted circumstances mythically, spoke deceptively, misunderstood economic dynamics, and steered the nation toward environmental destruction, debilitating debt and eventually endless world strife.

* The Carter/Reagan race was a watershed of American spirit. Reagan popularized resentment of the poor, distrust of government, hatred of taxes, contempt for science, environment, peace, social justice. He encouraged profligate consumption of nonrenewable resources, pollution, overpopulation, job outsourcing. For example, he imposed a gag rule on US-supported family planning, removed family planning from foreign aid, contemptuously ripped solar panels from the White House, appointed anti-environmentalist James Watt to Interior, encouraged Americans to buy big cars. He exposed American workers excessively to competition from foreign low-wage workers unencumbered by environmental rules and to illegal immigrants (amnesty), as part of his successful strategy to slow inflation by castrating our labor movement. Union membership declined, and homelessness rose steeply under Reagan and Bush I--quite a price for reduced inflation. He made objective discussion of taxes the true third rail of American politics.

* He single-handedly created the intellectual environment fertile for Rush Limbaugh, Grover Norquist, Dick Cheney, Jack Abramoff, K-Street Project, Bush II, Drill Drill Drill, Tea Party, Citizens United, Rick Santorum, Glen Beck, Sean Hannity, Mark ***. Owing to this legacy, it is no longer possible to have a rational national conversation about any public policy.

* Fox talk-radio hosts, Republican politicians and conservative think tanks regularly misrepresent Reagan's economic legacy.

* For example, they claim that his reduction of the top marginal income-tax rate from 70% to 50% or less actually increased income-tax revenue. They postulate that people avoided high tax brackets by withholding work effort, so eliminating the highest brackets unleashed their economic potential hence raised their tax payments and those of their employees and suppliers. This postulate underlies the Laffer Curve, which was said to have influenced Reagan's tax policies. Truth is, in these days of high productivity, coasting to avoid a high tax bracket would result in better sharing of economic activity, not less economic activity.

* In fact, Reagan's tax policies resulted in a 20% fall of income-tax revenue relative to Gross Domestic Product (GDP), despite reduction or closing of some deductions and loopholes (see also Fig 5); and his trade, labor, monetary and fiscal policies reduced fractional GDP growth rate by half, from 10% per year during several decades before 1983 to 5% per year after 1983 (see also Fig 1). GDP today is about 1/4 what it would have been without the Reagan revolution, and tax revenue is about 1/5 what it would have been without the revolution. After Reagan's tax cuts, it took about 4 years for tax revenue to return to pre-tax-cut levels. It would have taken 2 years were it not for Reagan's slowing of GDP growth.

* Between WWII and Reagan's presidency, the federal debt relative to GDP fell gradually from 1.2 to 0.35. This debt/GDP ratio then doubled during Reagan's and Bush I's administrations to 0.7 (owing to a quadrupling of debt with a doubling of GDP). It then declined to 0.6 during the Clinton years (tech bubble and increased tax rate) and then jumped to 1.05 (near bankruptcy) during the recent recession (see also Figs 3 &5). Had GDP continued growing as it did before the Reagan revolution, our debt/GDP ratio today would be less than 0.3, a perfectly safe value, less than 0.2 without the tax cuts.

* Of the debt quadrupling under Reagan and Bush I, the increases were 2.7x under Reagan and 1.5x under Bush I. Thus, Reagan's debt was almost twice that of all previous presidents combined. His repeated campaign claim, that he could cut taxes and increase spending while balancing the budget, was a lie that seems to have been forgiven and forgotten when the Ronald Reagan Legacy Project was getting schools, streets and an airport named for the man. The massive Reagan debt had two main components. About half was due to tax cuts and went to enrich the already rich. About half was due to increased spending and showed up in the military-industrial complex. Most of the debt was elective and could have been avoided.

* Reagan believed that the economy was unsatisfactory for lack of capital. It was for lack of consumer capacity (incident to high oil price), which could have been relieved by government spending on projects to reduce oil dependence (see also Fig 2). Reagan's tax, labor, regulatory and trade policies then caused a massive transfer of wealth and power from American workers to already wealthy Americans (see Fig 4) and to foreign and global interests. The shift of wealth to the already wealthy far exceeded that needed for capital formation, so unproductive speculative instruments were invented to occupy the excess. I don't think any of the above Reagan effects are laudable. Nevertheless, those policies helped bridle inflation (see Fig 1) and woke up the Dow after two decades of quiescence--good for those of us who saved systematically for decades before 1990.

* Ford and Carter were victims and Reagan was beneficiary of oil-producer actions to raise crude price from $16/barrel to $74/barrel between 1973 and 1981. Failure of OPEC discipline and efficiencies implemented under Carter then led to a gradual fall of crude price to $20/barrel between 1981 and 1987 where it remained until it rose sharply to $95/barrel during Bush II's administration (see Fig 2). Those oil-price swings caused corresponding swings of inflation, interest rates, unemployment and misery index (except during the recent housing bubble) (see Figs 1 & 2). This dynamic along with the hostage crisis defeated Carter and gave Reagan credit for improvements he did not influence. In particular, unemployment and misery declined with minor bumps from 1981 to 2000 following the price of oil.

* Some observers credited Reagan's military buildup, especially "Star Wars", with the fall of the Soviet Union. More likely it was demoralization of the Soviet army in Afghanistan, fugacity of tribes mingled in the union, attraction to western opulence, food insecurity due to the falling oil price (see also Fig 2) and to losing as innovators and producers in the global market.

* Why does this matter? In 1980 America was poised to lead the world in development, manufacture and deployment of solar voltaics and wind turbines. We could have led the world in responsible reproductive mores, resource husbanding, waste management and juster sharing of life's satisfactions. Reagan abdicated that kind of leadership and turned our future over to global market forces. There were 4.5 billion people back then, more than 7 billion now, about 1/5 not sure of eating tomorrow. Smart phones, millions of unemployed middle-class graduates and government policies concentrating wealth in the financial-service industry constitutes an incendiary Reaganomic mixture. Obama's failure to appreciate the rationale of his presidency with respect to these dynamics probably accounts for the Occupy movement.

* Conventional wisdom holds that Jimmy Carter failed as president and Ronald Reagan succeeded. At the time, it seemed to me that Carter interpreted circumstances objectively, spoke candidly, understood economic dynamics, and steered the nation appropriately into the future. It seemed to me that Reagan interpreted circumstances mythically, spoke deceptively, misunderstood economic dynamics, and steered the nation toward environmental destruction, debilitating debt and eventually endless world strife.

* The Carter/Reagan race was a watershed of American spirit. Reagan popularized resentment of the poor, distrust of government, hatred of taxes, contempt for science, environment, peace, social justice. He encouraged profligate consumption of nonrenewable resources, pollution, overpopulation, job outsourcing. For example, he imposed a gag rule on US-supported family planning, removed family planning from foreign aid, contemptuously ripped solar panels from the White House, appointed anti-environmentalist James Watt to Interior, encouraged Americans to buy big cars. He exposed American workers excessively to competition from foreign low-wage workers unencumbered by environmental rules and to illegal immigrants (amnesty), as part of his successful strategy to slow inflation by castrating our labor movement. Union membership declined, and homelessness rose steeply under Reagan and Bush I--quite a price for reduced inflation. He made objective discussion of taxes the true third rail of American politics.

* He single-handedly created the intellectual environment fertile for Rush Limbaugh, Grover Norquist, Dick Cheney, Jack Abramoff, K-Street Project, Bush II, Drill Drill Drill, Tea Party, Citizens United, Rick Santorum, Glen Beck, Sean Hannity, Mark ***. Owing to this legacy, it is no longer possible to have a rational national conversation about any public policy.

* Fox talk-radio hosts, Republican politicians and conservative think tanks regularly misrepresent Reagan's economic legacy.

* For example, they claim that his reduction of the top marginal income-tax rate from 70% to 50% or less actually increased income-tax revenue. They postulate that people avoided high tax brackets by withholding work effort, so eliminating the highest brackets unleashed their economic potential hence raised their tax payments and those of their employees and suppliers. This postulate underlies the Laffer Curve, which was said to have influenced Reagan's tax policies. Truth is, in these days of high productivity, coasting to avoid a high tax bracket would result in better sharing of economic activity, not less economic activity.

* In fact, Reagan's tax policies resulted in a 20% fall of income-tax revenue relative to Gross Domestic Product (GDP), despite reduction or closing of some deductions and loopholes (see also Fig 5); and his trade, labor, monetary and fiscal policies reduced fractional GDP growth rate by half, from 10% per year during several decades before 1983 to 5% per year after 1983 (see also Fig 1). GDP today is about 1/4 what it would have been without the Reagan revolution, and tax revenue is about 1/5 what it would have been without the revolution. After Reagan's tax cuts, it took about 4 years for tax revenue to return to pre-tax-cut levels. It would have taken 2 years were it not for Reagan's slowing of GDP growth.

* Between WWII and Reagan's presidency, the federal debt relative to GDP fell gradually from 1.2 to 0.35. This debt/GDP ratio then doubled during Reagan's and Bush I's administrations to 0.7 (owing to a quadrupling of debt with a doubling of GDP). It then declined to 0.6 during the Clinton years (tech bubble and increased tax rate) and then jumped to 1.05 (near bankruptcy) during the recent recession (see also Figs 3 &5). Had GDP continued growing as it did before the Reagan revolution, our debt/GDP ratio today would be less than 0.3, a perfectly safe value, less than 0.2 without the tax cuts.

* Of the debt quadrupling under Reagan and Bush I, the increases were 2.7x under Reagan and 1.5x under Bush I. Thus, Reagan's debt was almost twice that of all previous presidents combined. His repeated campaign claim, that he could cut taxes and increase spending while balancing the budget, was a lie that seems to have been forgiven and forgotten when the Ronald Reagan Legacy Project was getting schools, streets and an airport named for the man. The massive Reagan debt had two main components. About half was due to tax cuts and went to enrich the already rich. About half was due to increased spending and showed up in the military-industrial complex. Most of the debt was elective and could have been avoided.

* Reagan believed that the economy was unsatisfactory for lack of capital. It was for lack of consumer capacity (incident to high oil price), which could have been relieved by government spending on projects to reduce oil dependence (see also Fig 2). Reagan's tax, labor, regulatory and trade policies then caused a massive transfer of wealth and power from American workers to already wealthy Americans (see Fig 4) and to foreign and global interests. The shift of wealth to the already wealthy far exceeded that needed for capital formation, so unproductive speculative instruments were invented to occupy the excess. I don't think any of the above Reagan effects are laudable. Nevertheless, those policies helped bridle inflation (see Fig 1) and woke up the Dow after two decades of quiescence--good for those of us who saved systematically for decades before 1990.

.svg){kind=link}

* Ford and Carter were victims and Reagan was beneficiary of oil-producer actions to raise crude price from $16/barrel to $74/barrel between 1973 and 1981. Failure of OPEC discipline and efficiencies implemented under Carter then led to a gradual fall of crude price to $20/barrel between 1981 and 1987 where it remained until it rose sharply to $95/barrel during Bush II's administration (see Fig 2). Those oil-price swings caused corresponding swings of inflation, interest rates, unemployment and misery index (except during the recent housing bubble) (see Figs 1 & 2). This dynamic along with the hostage crisis defeated Carter and gave Reagan credit for improvements he did not influence. In particular, unemployment and misery declined with minor bumps from 1981 to 2000 following the price of oil.

{kind=link}

{kind=link}

* Some observers credited Reagan's military buildup, especially "Star Wars", with the fall of the Soviet Union. More likely it was demoralization of the Soviet army in Afghanistan, fugacity of tribes mingled in the union, attraction to western opulence, food insecurity due to the falling oil price (see also Fig 2) and to losing as innovators and producers in the global market.

* Why does this matter? In 1980 America was poised to lead the world in development, manufacture and deployment of solar voltaics and wind turbines. We could have led the world in responsible reproductive mores, resource husbanding, waste management and juster sharing of life's satisfactions. Reagan abdicated that kind of leadership and turned our future over to global market forces. There were 4.5 billion people back then, more than 7 billion now, about 1/5 not sure of eating tomorrow. Smart phones, millions of unemployed middle-class graduates and government policies concentrating wealth in the financial-service industry constitutes an incendiary Reaganomic mixture. Obama's failure to appreciate the rationale of his presidency with respect to these dynamics probably accounts for the Occupy movement.

Subscribe to:

Comments (Atom)